Yesterday was payday for me, as in I was finally able to do my running around and deposit my paycheque, two days after the real payday. I had a good weekend and will be able to pay my bills, that much is certain, so it’s all good.

I was able to achieve the goals that I had set out for myself when I took that pause from my Long Term Savings plan. Namely, I am back above zero in my Main Account and my Mid-Term Savings is back to its minimal funding level (Namely $1k).

I will admit that this was with a bit of robbing Peter to pay Paul, but I did it to get my head on straight and back to where I feel somewhat comfortable, at least, not anxious and uneasy. It may seem a bit silly to stick to such arbitrary numbers, but this is what I have set for myself as the minimum I demand from (and for) myself.

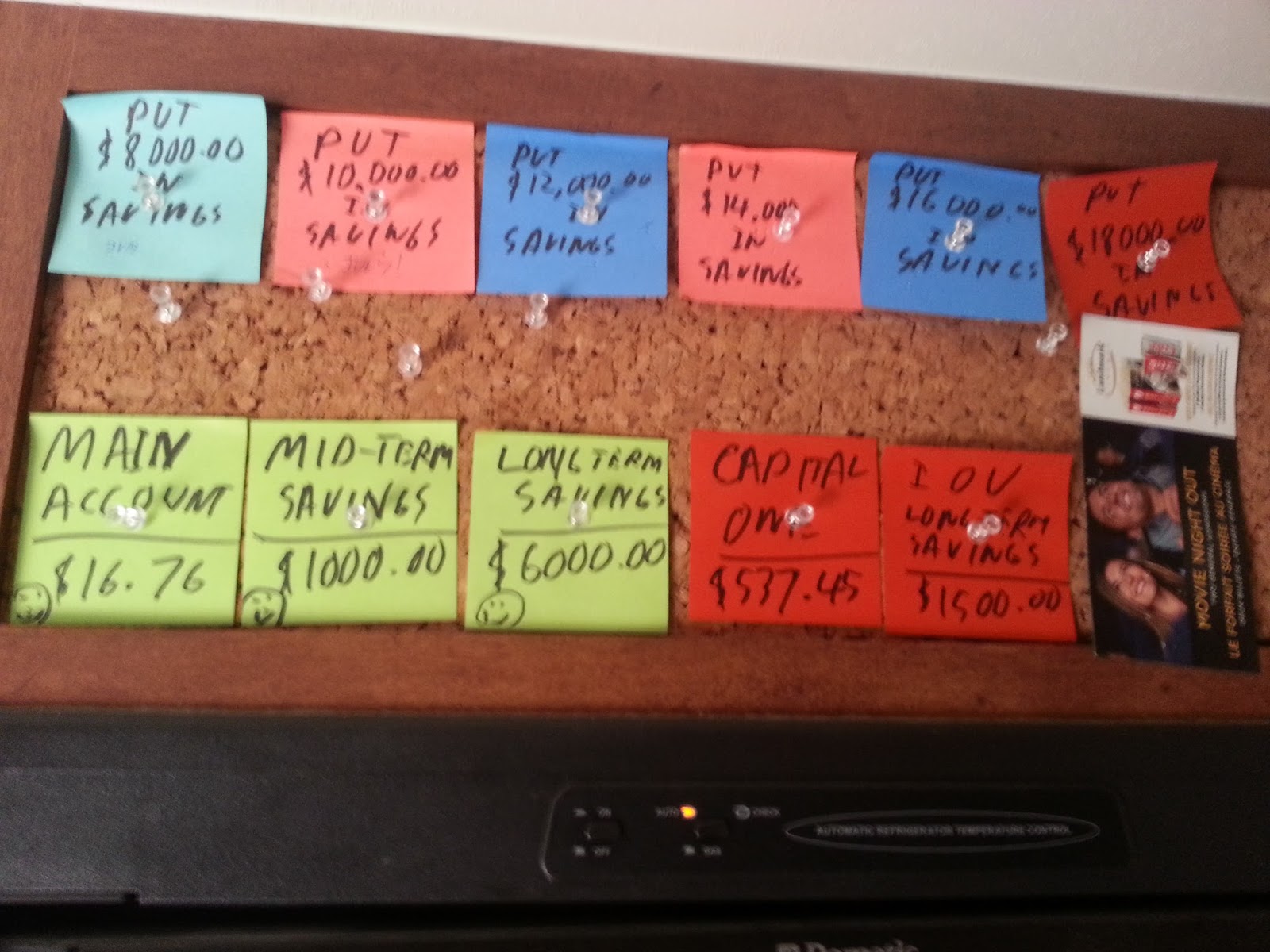

This is my motivation board that I use to keep myself on track and motivated. Across the top going from left to right are my savings goals. They are all broken down in easy and manageable $2000.00 increments.

By doing this, I get to see myself achieving smaller goals and set up a pattern that work towards my larger goals. If I achieve every one by the end of December, then I will be on track to pay Wanda off by December of next year (the big goal).

In the lower Left are the current statuses of my three accounts. This is to stare me in the face how I am actually doing. The happy faces shows that I am happy with how they are at the moment.

The Main Account shows only $16.76, and this is a bit of a misnomer. If I were to look at the bank balance of the Main Account, I would see a very different number, a much higher number, actually. This is due to the fact that since I consider $1k to be “Zero” for me, I subtract $1k from the bank balance.

Second of all, that is what the bank balance in the Main Account will be once all of my automatic bills and payments are paid. As in when I am standing there in the bank about to deposit the next paycheque, this is what will effectively be in the bank.

This is a key trick in budgeting, when thinking of what you have in your bank, don’t think about what is in there now, think about it in terms of once all of your bills have been paid. This way when you get the urge to spend you can look up and realize that you really have no extra cash to spend.

To the right of those “indicator notes” are two red notes; those are bills that I must pay, my Mid-Term bills. One is the one credit card that I put a bit on due to the vacation and a side project.

I plan to get this done in two paydays, three tops, all while keeping my savings plan on track and my butt above “Zero” in both my Main Account and Mid-Term Savings Account.

The other note is of course that IOU to my Long Term Savings Account that will need to be paid before December of this year, if I am to keep my top line goals on track.

It goes without saying that a life event may hit and all of this planning and these goals will go out the window. I can’t predict that, so all I can do is do what makes the most sense here and now and deal with whatever may come my way.

This is a demonstration of my “Dream for the future, Plan for the Mid-Term, yet work for the now” Moto.

I am Dreaming of saving a total of $36K by the end of December 2017, so I can pay off Wanda. In order to do that I am also Dreaming and Planning (Longer, Mid-Term) of saving up $18K this year and another $18k next year.

I am Planning to pay off the credit card first, and then after paying the Mid-Term Savings Account back for my Vacation (Namely, back up to $1k in it). After that I Plan to pay that IOU off, and hope to do it by the end of December this year.

In order to do all of that, I need to Focus on my budget and pay period cycle that I am in right now. I need to be able to not only to budget, but stick to that budget. If you can do that, consistently, then you can work towards anything and yes make your life better.

As always: Keep your head up, your attitude positive, and keep moving forward!

No comments:

Post a Comment